If you’ve ever tried implementing IFRS 9, you already know the truth: it’s not just an accounting change, it’s a data challenge. The calculations might look intimidating, but honestly? The real headache is getting your data house in order.

I’ve spent years helping organizations navigate IFRS 9 implementation, and I can tell you that the companies struggling the most aren’t the ones with complex loan portfolios. They’re the ones with messy data. Let’s talk about how to fix that.

Why Data Management Makes or Breaks IFRS 9 Compliance

Here’s the thing about IFRS 9, it’s hungry for data. And not just any data. It wants historical information, current details, and forward-looking estimates all wrapped together with a bow on top.

Think about what you need to calculate Expected Credit Loss (ECL):

- Complete borrower payment histories going back years

- Current loan balances and terms

- Credit ratings and how they’ve changed over time

- Collateral valuations

- Economic forecasts

- Industry performance metrics

And that’s just scratching the surface.

If your data is scattered across different systems, full of gaps, or inconsistent, you’re going to have a bad time. Actually, let me rephrase that you’re going to have an impossible time.

The Real Data Problems Nobody Talks About

Before we jump into solutions, let’s be honest about the problems. I’ve seen these issues at almost every organization I’ve worked with.

The Scattered Data Problem

Your loan origination data lives in one system. Your payment tracking is in another. Your credit ratings? That’s a spreadsheet someone updates manually. Customer information is in the CRM, but it doesn’t quite match what’s in the accounting system.

Sound familiar? You’re not alone. Most financial institutions grew their systems organically over decades, and now everything’s connected with digital duct tape and prayer.

The Historical Data Gap

IFRS 9 asks you to look back and analyze default patterns over multiple economic cycles. But what if you only started tracking certain data points three years ago? What if your system was replaced five years back and nobody migrated all the old records?

These gaps aren’t just inconvenient, they can seriously undermine your ECL calculations.

The Data Quality Nightmare

Here’s a fun game: check how many different ways your systems record a customer’s name. John Smith, J. Smith, Smith John, SMITH J—they’re all the same person, but try telling your database that.

Duplicate records, missing fields, inconsistent formats, outdated information… data quality issues multiply faster than rabbits.

The Forward-Looking Information Challenge

IFRS 9 requires forward-looking information. But how do you systematically incorporate economic forecasts into your data management framework? How do you track which forecast scenarios you used for which calculations?

Most organizations treat this as an afterthought, then panic during audit season.

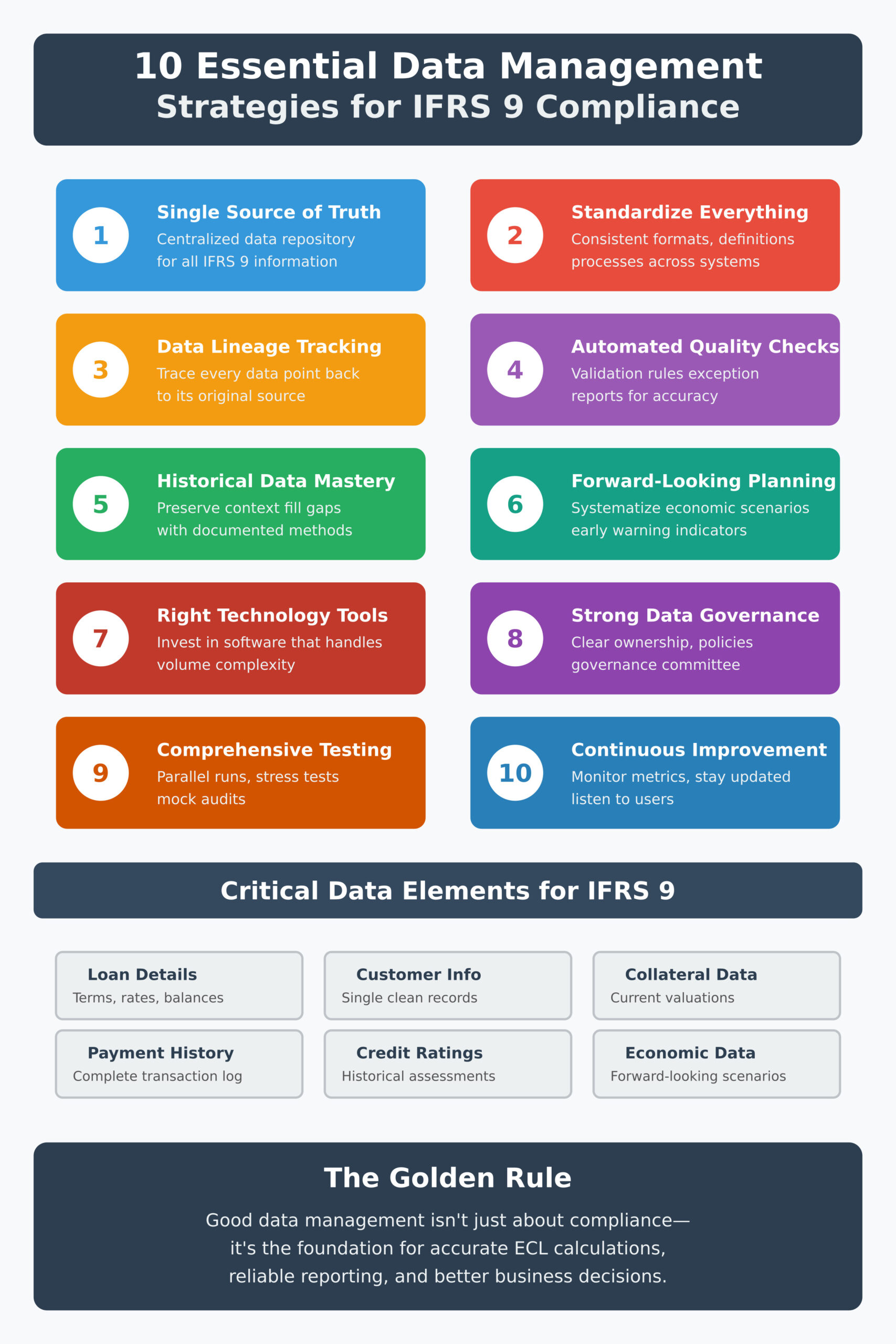

Strategy 1: Create a Single Source of Truth

Stop me if you’ve heard this before: “We’ll just pull data from all our systems when we need it.”

No. Just no.

You need a centralized data repository specifically designed for IFRS 9 compliance. Some people call it a data warehouse, others prefer “IFRS 9 data mart.” Call it whatever you want, but build it.

What Goes Into Your Data Repository

Your central repository should include:

Loan-level details: Every loan, every term, every modification. If it affects the cash flows or credit risk, it belongs here.

Customer information: One clean record per customer. No duplicates. Current contact details, employment status, financial information—everything that impacts creditworthiness.

Payment history: Complete payment records going back as far as you have them. Late payments, missed payments, prepayments—capture it all.

Stage classifications: Track which IFRS 9 stage each loan is in and when it moved between stages. This audit trail is crucial.

Credit assessments: Historical and current credit ratings, plus the methodology and date for each assessment.

Collateral data: Current valuations, appraisal dates, and collateral type for secured loans.

Economic data: The forward-looking information you’re using, including GDP forecasts, unemployment rates, interest rate projections, and industry-specific indicators.

Keep It Updated, Keep It Clean

A data repository is only useful if it’s current. Set up automated feeds from your source systems. Daily updates for transactional data like payments. Weekly or monthly updates for things that change less frequently.

And please, implement data validation rules at the point of entry. It’s much easier to prevent bad data from getting in than to clean it up later.

Strategy 2: Standardize Everything You Can

Consistency is your friend in IFRS 9 compliance.

Standard Data Formats

Pick one format for dates and stick with it everywhere. Same goes for currency formatting, customer identifiers, product codes, and everything else.

I once worked with a bank that had three different systems recording loan amounts. One used two decimal places, another used four, and the third rounded to the nearest whole number. Guess how much fun reconciliation was? Not fun. Not fun at all.

Standard Definitions

What counts as a “default” in your organization? When does a payment become “past due”? How do you define “significant increase in credit risk”?

Write these definitions down. Make sure everyone and I mean everyone uses the same definitions. Your loan officers, your credit team, your IT department, your compliance folks. Everyone.

These definitions should be coded into your systems so they’re applied consistently every single time.

Standard Processes

Document your data collection processes. Who’s responsible for updating customer information? How often do you revalue collateral? What’s the approval process for stage migrations?

Standard processes mean consistent data, which means reliable ECL calculations.

Strategy 3: Build Comprehensive Data Lineage

Pop quiz: A regulator asks you to explain exactly how you calculated the ECL for a specific loan portfolio. Can you trace every data point back to its source?

If you hesitated, you need better data lineage.

Track the Journey

For every piece of data in your IFRS 9 calculations, you should be able to answer:

- Where did it come from originally?

- When was it collected or calculated?

- Has it been transformed or adjusted? How?

- Who approved it?

- What assumptions went into it?

This isn’t just about compliance (though auditors absolutely love good data lineage). It’s about understanding your own processes well enough to spot problems early.

Document Your Transformations

Maybe you’re taking raw payment data and calculating days past due. Or you’re converting credit scores from one scale to another. Perhaps you’re adjusting historical default rates for current economic conditions.

Whatever transformations you’re doing, document them. Write down the formulas. Explain the business logic. Make it so clear that someone new to your organization could follow the process.

Strategy 4: Automate Data Quality Checks

Manual data quality reviews are important, but they’re not enough. You need automated checks running constantly in the background.

Set Up Smart Validation Rules

Build validation rules that catch problems automatically:

Completeness checks: Flag records with missing required fields. If a loan doesn’t have an origination date or interest rate, something’s wrong.

Range checks: Interest rates should fall within reasonable bounds. A 150% interest rate on a mortgage? That’s probably a data entry error.

Consistency checks: The total of individual loan balances should match the portfolio total. If they don’t, investigate immediately.

Timing checks: Payment dates should come after loan origination dates. Sounds obvious, but you’d be surprised how often this gets messed up.

Cross-system validation: Does the customer name in your loan system match the CRM? Do loan balances tie back to the general ledger?

Create Exception Reports

Your automated checks should generate exception reports highlighting issues that need human review. But here’s the key—make these reports actionable.

Don’t just say “147 records failed validation.” Say “147 loans are missing collateral valuations. Owner: Maria Garcia. Due date for resolution: Friday.”

Assign ownership. Set deadlines. Track resolution. Otherwise, those exception reports will pile up unread in someone’s inbox.

Strategy 5: Master Historical Data Management

IFRS 9 is all about learning from the past to predict the future. That means your historical data needs to be rock solid.

Fill the Gaps Thoughtfully

Maybe you don’t have complete historical data. That’s okay—many organizations don’t. But you need a plan for dealing with gaps.

Can you use proxy data from similar loan portfolios? Can you reference industry benchmarks? Can you work with data you do have and clearly document the limitations?

Whatever approach you choose, be consistent and transparent about it.

Preserve Context

Don’t just store raw numbers—store the context around them. Why did 20 customers default in Q3 2020? Because there was a pandemic affecting their industries.

That context matters when you’re trying to determine whether historical patterns will repeat.

Version Control Matters

Your ECL model parameters will change over time. Your economic forecasts will be updated quarterly. When you look back at last year’s calculations, you need to know exactly what data and assumptions you used.

Implement version control for your data sets, just like software developers do for code. Each quarter’s calculations should reference specific, timestamped versions of your data.

Strategy 6: Plan for Forward-Looking Information

IFRS 9’s forward-looking requirement is tough because you’re essentially trying to organize data about the future. Fun, right?

Systematize Economic Scenario Management

Don’t let economic scenarios live in someone’s head or scattered across email threads. Create a formal process:

Source your forecasts from reputable providers, government agencies, central banks, recognized economic research firms.

Document your scenarios: base case, optimistic, pessimistic. What are the specific assumptions? What’s the probability weighting for each?

Store scenarios systematically: Each scenario should be dated, sourced, and version-controlled.

Link scenarios to calculations: Your ECL calculations should reference specific scenario versions so you can recreate them later.

Create Early Warning Indicators

Set up a dashboard tracking leading economic indicators relevant to your portfolio. When these indicators start flashing red, you know it’s time to update your forward-looking assumptions.

For a bank with heavy real estate exposure, you might track housing starts, mortgage rates, and regional employment data. For an auto lender, you’d watch consumer confidence and gas prices.

Make this data easily accessible to your credit risk team so they can adjust models proactively rather than reactively.

Strategy 7: Invest in the Right Technology

Let’s talk tools. You’re not going to manage IFRS 9 data successfully in Excel. I mean, you could try, but please don’t.

What to Look for in IFRS 9 Data Management Software

You need IFRS 9 compliance software that can:

Integrate data from multiple source systems without requiring a PhD to set up.

Handle large volumes efficiently. If you have hundreds of thousands of loans, your system needs to process them without grinding to a halt.

Support complex calculations including probability of default, loss given default, and exposure at default across different scenarios.

Maintain audit trails automatically. Every change, every calculation, every assumption should be logged.

Generate reports that both humans and regulators can understand.

Adapt to changes in your methodology without requiring a complete rebuild.

Cloud vs On-Premise

More organizations are moving to cloud-based solutions for IFRS 9 data management, and for good reason. Cloud platforms offer:

- Easier scalability when your data volumes grow

- Automatic updates and improvements

- Better disaster recovery capabilities

- Lower upfront costs (though ongoing subscription fees add up)

But if you’ve got regulatory constraints or security requirements that demand on-premise solutions, that’s fine too. Just make sure whatever you choose can actually handle your needs.

Strategy 8: Don’t Forget About Data Governance

Technology and processes are important, but people and policies hold everything together.

Establish Clear Data Ownership

Every critical data element in your IFRS 9 framework should have an owner—a specific person responsible for its accuracy and completeness.

Who owns customer credit ratings? Who’s responsible for collateral valuations? Who maintains the economic scenarios?

When everyone’s responsible, nobody’s responsible. Assign clear ownership.

Create a Data Governance Committee

Bring together representatives from IT, finance, risk management, and business units. This committee should:

- Review and approve data management policies

- Resolve data quality issues that cross departmental boundaries

- Prioritize data improvement initiatives

- Monitor compliance with data standards

Meet regularly—at least monthly during implementation, quarterly once you’re in steady state.

Document Everything

I know, I know. Documentation is boring. But it’s essential.

Document your data definitions, your processes, your system architecture, your validation rules, your transformation logic. Create a data dictionary that explains every field in your IFRS 9 repository.

When someone new joins your team, they should be able to read your documentation and understand how everything works. When auditors show up, you should be able to hand them clear documentation that answers their questions.

Strategy 9: Test, Test, and Test Again

Before you rely on your IFRS 9 data management framework for actual reporting, test it thoroughly.

Run Parallel Calculations

If you’re transitioning from a legacy system or process, run both the old and new approaches side by side for at least one full reporting cycle.

Compare results. Investigate differences. Make sure you understand why the numbers changed.

Stress Test Your Data

What happens if transaction volumes double? What if you need to add a new loan product with different characteristics? What if economic conditions change dramatically?

Test your data management framework under various scenarios to make sure it holds up.

Conduct Mock Audits

Have your internal audit team review your IFRS 9 data management processes before the external auditors show up. Better to find and fix problems internally than during a formal audit.

Strategy 10: Plan for Continuous Improvement

IFRS 9 compliance isn’t a one-time project, it’s an ongoing commitment. Your data management strategies need to evolve.

Monitor Performance Metrics

Track key metrics about your data management effectiveness:

- Data quality scores (percentage of records with no errors)

- Time required for month-end data preparation

- Number of data-related audit findings

- System performance and processing times

Set targets for improvement and track your progress over time.

Stay Updated on Standards

IFRS standards evolve. Interpretations get clarified. Best practices emerge. Stay connected to industry groups, attend conferences, participate in webinars.

When guidance changes, assess the impact on your data requirements and adjust accordingly.

Listen to Your Users

The people using your IFRS 9 data management framework every day—your analysts, your risk managers, your reporting team—they know where the pain points are.

Create feedback mechanisms so they can report issues and suggest improvements. Actually listen to them and implement good ideas.

Common Data Management Mistakes to Avoid

Let me save you some pain by highlighting mistakes I’ve seen organizations make repeatedly.

Mistake 1: Underestimating Data Preparation Time

“We’ll have all the data ready in a month” is usually code for “We’ll be frantically patching things together for the next six months.”

Data preparation typically takes 2-3 times longer than initially estimated. Plan accordingly.

Mistake 2: Ignoring Data Privacy Requirements

IFRS 9 compliance doesn’t exempt you from GDPR, CCPA, or other privacy regulations. Make sure your data management framework includes appropriate privacy protections, access controls, and data retention policies.

Mistake 3: Over-Engineering the Solution

Yes, you need robust data management. No, you don’t need a system that can handle every possible future scenario you might dream up.

Start with what you need for basic compliance, then enhance over time. Perfect is the enemy of done.

Mistake 4: Treating It as an IT Project

IFRS 9 data management is a business initiative that needs technology support—not a technology project that happens to involve some business requirements.

Your finance and risk teams need to be deeply involved in designing and implementing your data framework. IT builds what the business needs, not the other way around.

Mistake 5: Skimping on Training

You can have the best data management framework in the world, but if your team doesn’t know how to use it properly, you’ll still have problems.

Invest in comprehensive training for everyone who touches IFRS 9 data. Not just the technical stuff, but also the “why” behind your processes and controls.

Bringing It All Together

Managing data for IFRS 9 compliance doesn’t have to be overwhelming. Yes, it’s complex. Yes, it requires investment. But break it down into manageable strategies and tackle them systematically.

Start with a centralized data repository. Standardize your definitions and formats. Build in quality checks and validation. Document everything. Use the right technology. Establish clear governance. And keep improving over time.

The organizations that succeed with IFRS 9 are the ones that treat data management as a strategic priority, not an afterthought. They recognize that good data is the foundation for accurate calculations, reliable reporting, and ultimately, better credit risk management.

Your IFRS 9 journey might feel daunting right now, but with solid data management strategies in place, you’ll navigate it successfully. And who knows? You might even find that the improved data management capabilities you build for IFRS 9 help your organization in ways that extend far beyond compliance.

After all, good data isn’t just about satisfying regulators—it’s about making better business decisions. And that’s something every organization can benefit from.

Final Thoughts

If you take away just one message from this guide, let it be this: invest in your data infrastructure early. The time, money, and effort you spend getting your data house in order will pay dividends many times over.

IFRS 9 compliance might be what’s forcing you to tackle data management seriously, but the benefits will extend across your entire organization. Better risk assessment, more accurate forecasting, faster reporting, clearer audit trails, these advantages go way beyond just checking a compliance box.

Start where you are. Assess your current state honestly. Prioritize your biggest gaps. Build your data management capabilities step by step. And don’t try to do everything at once.

Remember, every organization implementing IFRS 9 has faced similar challenges. You’re not alone in this. Reach out to peers, learn from their experiences, and don’t be afraid to ask for help when you need it.

Good data management isn’t glamorous, but it’s absolutely essential. Get it right, and everything else about IFRS 9 compliance becomes much, much easier.

Author Bio: With over a decade of experience helping financial institutions implement IFRS 9 and strengthen their data management capabilities, I’ve seen firsthand what works and what doesn’t. This guide reflects lessons learned from dozens of implementations across different types and sizes of organizations. The goal is simple: help you avoid the mistakes others have made and build a data foundation that serves you well for years to come.